Parking Authority Appoints to Board

James S. Cassel

Week of Thursday, February 24

The Miami Parking Authority has appointed James S. Cassel to its board of directors.

Click here to read the PDF.

")

James S. Cassel

Week of Thursday, February 24

The Miami Parking Authority has appointed James S. Cassel to its board of directors.

Click here to read the PDF.

Offers Thousands of Products Through Large Format Stores with 2021 Revenue of $757 Million Provides Significant Revenue and Earnings Growth Opportunity Expected to be Accretive to Adjusted EBITDA and Non-GAAP EPS Immediately Following Closing

![]()

NEWS PROVIDED BY The Aaron’s Company, Inc. February 23, 2022

ATLANTA, Feb. 23, 2022 /PRNewswire/ — The Aaron’s Company, Inc. (“Aaron’s”) (NYSE: AAN), a leading technology-enabled, omnichannel provider of lease-to-own and purchase solutions, today announced that it has entered into a definitive agreement to acquire BrandsMart U.S.A. (“BrandsMart”). Under the terms of the agreement, total consideration is approximately $230 million in cash, subject to certain closing adjustments, and the transaction is expected to close in the second quarter of 2022. With this transaction, we believe that Aaron’s will deliver over $3 billion in total annual revenues and over $300 million in adjusted EBITDA by year-end 2026.

Founded in 1977, BrandsMart is one of the leading appliance and consumer electronics retailers in the southeast United States and one of the largest appliance retailers in the country with ten stores in Florida and Georgia and a growing e-commerce presence on brandsmartusa.com. The company offers best-in-class pricing, a wide selection of brands, and thousands of products, including large and small appliances, consumer electronics, computers, furniture and other home goods. BrandsMart’s value proposition has attracted a loyal and recurring customer base, resulting in revenue, EBITDA, and free cash flow growth. For the twelve months ended December 25, 2021, BrandsMart generated revenues of $757 million and Adjusted EBITDA of $46 million.

“We are thrilled to announce our agreement to acquire BrandsMart, which we believe strengthens Aaron’s ability to deliver on our mission of enhancing people’s lives by providing easy access to high-quality products through affordable lease and retail purchase options. The acquisition is expected to provide meaningful value-creation opportunities, which include leveraging Aaron’s lease-to-own expertise to provide BrandsMart customers enhanced payment options and offering a wide selection of BrandsMart’s product assortment to millions of Aaron’s customers. Importantly, we believe the acquisition of BrandsMart will expand our addressable market and create an additional platform for accelerated growth,” said Aaron’s CEO, Douglas Lindsay.

“We are excited to welcome BrandsMart to the Aaron’s family. We look forward to partnering with their experienced management team to expand the BrandsMart footprint, and we believe that the consolidated business can deliver strong revenue and double-digit annual adjusted EBITDA growth over the next five years and beyond,” Lindsay concluded.

BrandsMart’s President and Chief Executive Officer Michael Perlman said, “I am proud to share the momentous news that BrandsMart is joining the Aaron’s family of companies. BrandsMart has been part of my family for over 45 years, and I am incredibly proud of our team and the success of the company we have built together. I am confident that the combined organization will benefit from our complementary strengths and will deliver growth opportunities and even greater value to our customers, employees and suppliers.” Upon closing of the transaction, the BrandsMart business will report to Aaron’s President, Steve Olsen, and continue to be headquartered in Ft. Lauderdale, FL.

Compelling Strategic and Financial Benefits

Transaction Terms and Financing

Under the terms of the agreement, Aaron’s will acquire 100% of the outstanding equity interests of Interbond Corporation of America, which does business as BrandsMart U.S.A., from the Perlman family for consideration at closing of $230 million in cash, subject to certain post-closing adjustments. The transaction is intended to be funded through a combination of cash on hand and debt financing.

In connection with the transaction, Aaron’s has secured a $200 million financing commitment from Truist Bank, Bank of America, N.A., JPMorgan Chase Bank, N.A. and Citizens Bank, N.A., each of which is a lender in our existing senior unsecured credit facility. The financing commitment is expected to be structured as a term loan, maturing on November 9, 2025, with an initial interest rate of SOFR (Secured Overnight Financing Rate) plus 1.75%.

Conference Call and Webcast

Aaron’s will hold a conference call to discuss its quarterly results and the acquisition of BrandsMart on February 24, 2022, at 8:30 a.m. Eastern Time. The public is invited to listen to the conference call by webcast accessible through Aaron’s investor relations website, investor.aarons.com. The webcast will be archived for playback at that same site. An investor presentation related to Aaron’s agreement to acquire BrandsMart can be found on Aaron’s investor site at investor.aarons.com. Advisors BofA Securities, Inc. is acting as financial advisor to Aaron’s and Jones Day is acting as legal advisor. Cassel Salpeter & Co., LLC is acting as financial advisor to BrandsMart and Cooley LLP is acting as legal advisor.

About The Aaron’s Company

Headquartered in Atlanta, The Aaron’s Company, Inc. (NYSE: AAN) is a leading omnichannel provider of lease-to-own and purchase solutions. Aaron’s engages in direct-to-consumer sales and lease ownership of furniture, home appliances, consumer electronics and accessories through its approximately 1,300 company-operated and franchised stores in 47 states and Canada, as well as its e-commerce platform, Aarons.com. For more information, visit Aarons.com or investor.aarons.com.

About BrandsMart USA

BrandsMart USA is one of the leading appliance and consumer electronics retailers in the southeast United States and one of the largest appliance retailers in the country with ten retail stores in Florida and Georgia and a growing ecommerce presence at brandsmartusa.com. The company offers hundreds of name brands across thousands of different items, including large and small appliances, consumer electronics, computers, furniture, and home goods. For more information, visit brandsmartusa.com.

Forward-Looking Statements

Statements in this news release regarding our business that are not historical facts are “forward-looking statements” that involve risks and uncertainties which could cause actual results to differ materially from those contained in the forward-looking statements. Such forward-looking statements generally can be identified by the use of forward-looking terminology, such as “remain,” “believe,” “outlook,” “expect,” “assume,” “assumed,” and similar terminology. These risks and uncertainties include factors such as (i) any ongoing impact of the COVID19 pandemic due to new variants or efficacy and rate of vaccinations, as well as related measures taken by governmental or regulatory authorities to combat the pandemic; (ii) the occurrence of any event, change or other circumstances that could give rise to the termination of the purchase agreement related to the proposed acquisition; (iii) the risk that the necessary regulatory approvals may not be obtained or may be obtained subject to conditions that are not anticipated; (iv) the risk that the proposed acquisition will not be consummated in a timely manner or at all; (v) risks that any of the closing conditions to the proposed acquisition may not be satisfied or may not be satisfied in a timely manner; (vi) risks related to the disruption of management time from ongoing business operations due to the proposed acquisition; (vii) failure to realize the benefits expected from the proposed acquisition, including projected synergies; (viii) failure to promptly and effectively integrate the proposed acquisition; (ix) the effect of the announcement of the proposed acquisition on our operating results and businesses and on the ability of Aaron’s and BrandsMart to retain and hire key personnel, maintain relationships with suppliers; (x) the risks associated with our strategy and strategic priorities not being successful, including our e-commerce and real estate repositioning and optimization initiatives or being more costly than anticipated; (xi) our ability to adjust pricing to offset, or partially offset, inflationary pressure on the cost of our products and services; (xii) supply chain delays and disruptions, including adverse consequences to our supply chain function from decreased procurement volumes and from the COVID-19 pandemic; and (xiii) the other risks and uncertainties discussed under “Risk Factors” in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2021 and any subsequent reports filed with the Securities and Exchange Commission. Statements in this press release that are “forward-looking” include without limitation statements with respect to the Company’s goals, plans, expectations, projections regarding the expected benefits of the proposed acquisition, management’s plans, projections and objectives for the proposed acquisition, future operations, scale and performance, integration plans and expected synergies therefrom, the timing of completion of the proposed acquisition, and our financial position, results of operations, market position, capital allocation strategy, initiatives, business strategy and expectations of our management following the completion of the proposed acquisition. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this press release. Except as required by law, the Company undertakes no obligation to update these forward-looking statements to reflect subsequent events or circumstances after the date of this press release.

SOURCE The Aaron’s Company, Inc.

Click here to read the PDF.

Click here to read the full article.

Committed to providing world-class independent investment banking services to middle-market and emerging growth companies, Cassel Salpeter is pleased to announce the promotions of Laura Salpeter from vice president to director and Tahz Rashid from analyst to associate.

By E. Napoletano, Contributor

February 16, 2022

On Feb. 1, the U.S. Treasury Department reported that the U.S. gross national debt surpassed $30 trillion for the first time, a figure that’s incomprehensible at the best of times, let alone when many Americans are still dealing with the economic impact of the coronavirus pandemic.

But as unfathomable as this number is, the national debt can impact ordinary

Americans’ lives.

Daniel Rodriguez, COO at Hill Wealth Strategies, says that if the government wants to maintain the same level of benefits and services to Americans and its international allies without running up both the deficit and the national debt, more revenue will be required.

“The only way to get more revenue is to increase taxes on the American people or reduce spending,” he says. “The government may choose to reduce spending on things like infrastructure, social safety nets, first responders, and education. Those programs have direct impacts on Americans’ day-to-day lives.”

Here’s what the national debt is, the factors responsible for making it rise and fall and how it can impact your life.

What Is the National Debt?

Just like the debt you have is a figure that represents how much you owe your creditors, the national debt represents how much the United States government owes its creditors.

When the U.S. government spends more money than the revenues it brings in each year, it creates an imbalance called a budget deficit. The government must then borrow money to cover its expenses.

It’s more common than not for the government to run a deficit, regardless of which party is in charge. In fact, the government has run a deficit for 77 of the past 90 years and first carried debt after the Revolutionary War in 1790.

How Could the National Debt Impact Consumers?

Congress is responsible for ensuring the government stays funded, but you might still be curious about the national debt and how it relates to the federal deficit.

Here are six ways the rising national debt could potentially impact Americans.

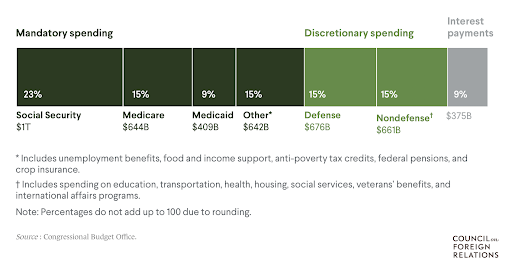

Source: Congressional Budget Office

What Causes the National Debt to Increase?

Sometimes the government needs to increase spending to stabilize the economy, and protect Americans and businesses from unexpected economic conditions.

During The Great Recession (Dec. 2007 to Jun. 2009), for example, Congress passed legislation injecting $1.8 trillion into the economy. But that pales in comparison to the $4.5 trillion the Trump and Biden administrations have pumped into the economy since the Covid pandemic began in March 2020. However, there are other reasons the national debt increases, even during years where spending is moderate and the economy is in good shape

Tax Cuts

On one hand, tax cuts can stimulate the economy and put more money in Americans’ bank accounts every payday. But those same tax cuts mean the federal government brings in less revenue across the board.

For example, the Tax Cuts and Jobs Act of 2017 slashed taxes for individual and corporate payers, but created a $275 billion shortfall in revenue even though the economy grew. The Act caused revenue from corporate taxes to decrease by $135 billion, a 40% reduction from projected revenue.

Rising Healthcare Costs

According to data from the nonpartisan Peter G. Peterson Foundation, per capita healthcare spending in the U.S. is three times higher than in comparable developed nations like the United Kingdom and France. As America’s population ages, more people enroll in Medicare—and older Americans typically require more care. This translates to the federal budget bearing the burden for rising healthcare costs.

Interest Costs

If you’ve ever had a car loan or mortgage, you’re familiar with how much of your payment each month goes toward interest. The same is true of the federal government’s debts. As the national debt rises, the government will pay more interest to keep those debts in good standing.

Using data from the Congressional Budget Office and the Office of Management and Budget, the Peter G. Peterson Foundation estimates that the government will pay a staggering $5.4 trillion in interest over the next 10 years.

Who’s Responsible for the Current National Debt?

In short? Pretty much every administration.

“Regardless of political affiliation, parties in power have run up the deficit through higher spending and lower revenue collection,” says Brian Rehling, head of Global Fixed Income Strategy at Wells Fargo Investment Institute.

While it’s easy to say a particular president or president’s administration caused the federal deficit and national debt to move a certain direction, it’s important to note that only Congress can authorize the type of legislation with the most impact on both figures.

Here’s a look at how Congress acted during four notable presidential administrations and how their actions impacted both the deficit and national debt.

Franklin D. Roosevelt

As the nation’s last four-term president, FDR helped Americans weather an abundance of economic crises. His presidency spanned The Great Depression and his signature New Deal economic recovery package helped lift America out of financial rock bottom. But the most significant increase to the national debt was the cost of World War II, which added roughly $186 billion to the national debt between 1942 and 1945. Congress added $236 billion to the national debt during FDR’s terms, representing an increase of 1,048%.

Ronald Reagan

During Reagan’s two terms, Congress enacted two historic tax cuts that decreased government revenue: the Economic Recovery Tax Act of 1981 and the Tax Reform Act of 1986. These Acts passed by Congress decreased revenue as a percent of the GDP by 1.7% between 1982 and 1990, creating a revenue shortfall that contributed to the national debt increasing 261% ($1.26 trillion) during his administration, from $924.6 billion to $2.19 trillion.

Barack Obama

Over two terms, the Obama administration oversaw both The Great Recession due to the collapse of the mortgage market and the ensuing recovery. In 2009, Congress passed the Economic Stimulus Act, which helped countless Americans save their homes from foreclosure, pumping $831 billion into the economy. Congressional tax cuts accounted for another $858 billion added to the national debt when passed by a strong bipartisan showing. All in all, Congressional action increased the national deficit by 74 percent and added $8.6 trillion to the national debt during Obama’s two terms.

Donald Trump

During his single term, Congress passed the Tax Cuts and Jobs Act in 2017, which slashed corporate and personal income tax rates. Considered by many a boon for the wealthiest Americans and corporations, at the time of its passage, the Congressional Budget Office estimated the cuts would increase the federal deficit by $1.9 trillion.

While the Treasury Secretary estimated that the tax cuts would decrease the federal deficit, the deficit increased from $665 billion in 2017 to $3.13 trillion in 2020. The tax cuts drove some of this increase but multiple Covid relief packages were responsible for the majority of the increase.

The federal debt held by the public increased from $14.6 trillion in 2017 to over $21 trillion in 2020. Public debt and intragovernmental debt (the amount owed to federal retirement trust funds like the Social Security Trust Fund) make up the national debt. It’s the amount of money the U.S. owes to outside debtors such as U.S. banks and investors, businesses, individuals, state and local governments, Federal Reserve and foreign governments and international investors like Japan and China. The money is borrowed to raise the cash needed to keep the U.S. operating. It includes Treasury bills, notes, and bonds. Other holders of public debt include Treasury Inflation-Protected Securities (TIPS), U.S. savings bonds and state and local government series securities.

“The national debt continues to grow as it has not for decades,” says James Cassel, chairman and co-founder of investment bank Cassel Salpeter. “This is the result of this simple concept of spending more money than you have in revenue.” Cassel also mentions that both major political parties have, at times, spoken seriously about a commitment to reduce the national debt yet conversations and strategy remain stalled.

However, the national debt is more commonly used as a bargaining chip when both parties posture about raising the debt ceiling each year. Without raising the debt ceiling, the U.S. would default on its debt obligations. Thus, Congress always votes to raise the debt ceiling (how much money the U.S. government can borrow), but not before parties negotiate on other legislation.

Are We Helpless When It Comes to the National Debt?

In some ways, yes. But there are actions you can take to mitigate the effect of the national debt on your life.

Rehling from Wells Fargo Investment Institute says that while the national debt has increased substantially over the past decade, the U.S. isn’t unique in this regard. The rest of the developed world has seen similar trends. “While these budget trends are unsustainable over the long run, there is no indication that current debt levels are overly worrisome,” he says.

Ed. note: This article has been corrected to more accurately reflect the U.S. national debt increased numbers.

Miami Investment Banking Firm Cassel Salpeter Issues Aviation Industry Deal Report

South Florida firm publishes Q4 2021 Aviation Deal Report surveying year’s company M&A, deal flow, and market trends

As Cassel Salpeter & Co. looks back on more than a decade of providing superior financial advisory services, we continue to grow in market intelligence, experience, and quality of personnel, refining our capabilities for the businesses we serve.